Latin America has long been rich in natural resources, and for much of its history, those resources have been presented as a promise of progress. In the nineteenth century, Peru and Chile occupied a privileged position in the global economy because they controlled something the industrial world desperately needed: nitrogen. First through guano exported from Peruvian islands, and later through nitrates mined in the Atacama Desert, these countries became essential suppliers for global agriculture and warfare. Revenues were enormous, state budgets expanded rapidly, and foreign capital poured in. From the outside, it looked like development was inevitable.

But prosperity based on extraction alone proved fragile. Despite decades of booming exports, neither Peru nor Chile used these resources to build diversified economies, strong technological capabilities, or inclusive social systems. Instead, wealth flowed outward through foreign firms, while states focused on collecting revenues rather than transforming production. When deposits were exhausted or global technology changed, fiscal crises, unemployment, and social instability followed. What had seemed like national success quickly became national vulnerability.

This blog revisits the guano and nitrate booms not as distant historical curiosities, but as early warnings. By examining how these industries were organized—who controlled them, how labor was used, where profits went, and what institutions were built—we can better understand why extraordinary resource wealth failed to deliver long-term development. For today’s policymakers and citizens in Latin America and the Caribbean, these cases raise a critical question that remains unresolved: how can the region turn natural wealth into lasting economic and social capacity, rather than repeating cycles of boom and collapse?

From Islands to Desert: The Rise of Latin America’s Nitrogen Economy

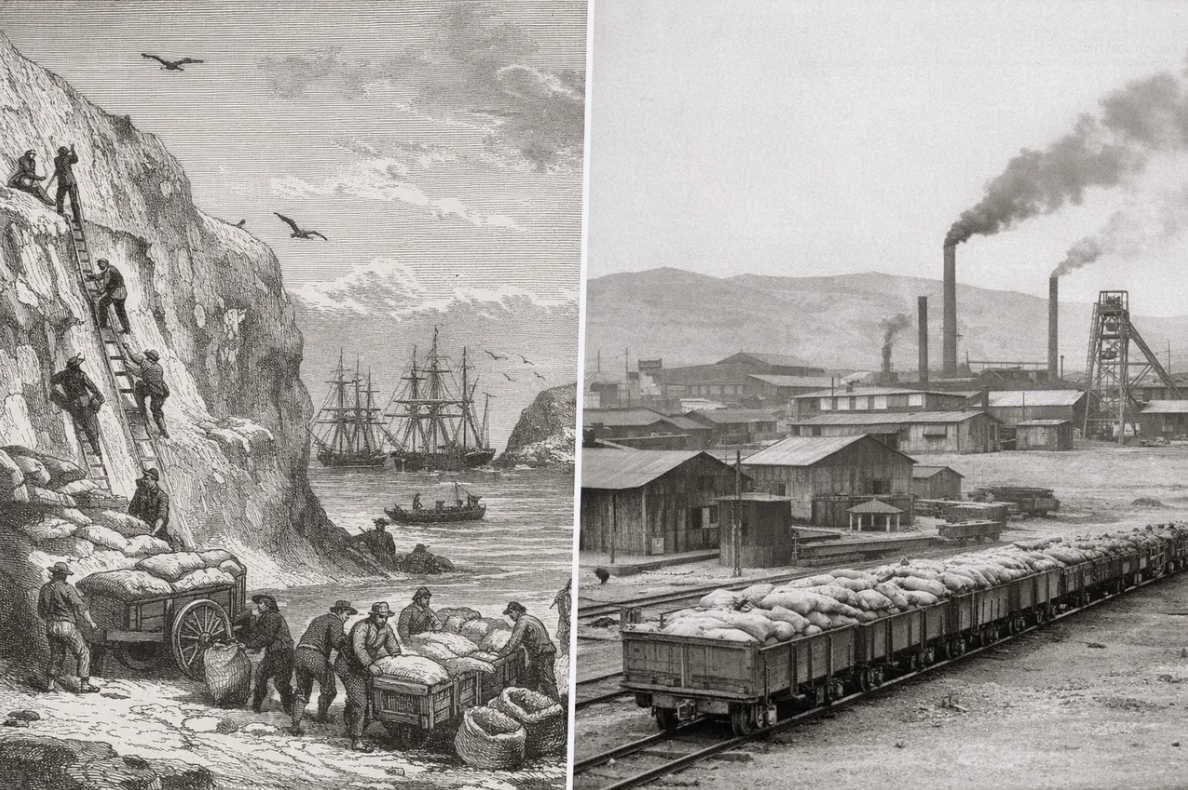

Between the 1840s and 1860s, guano extracted from Peruvian coastal islands functioned as the dominant global source of industrial nitrogen fertilizer. Approximately 11–12 million tons were exported between 1840 and 1870, financing most Peruvian public expenditures during this period. The production system was based on rapid physical depletion rather than renewable management, leading to a collapse of the resource base beginning in the 1860s. Labor inputs were coercive and low-skilled, relying on convicts, indigenous laborers, and roughly 100,000 Chinese indentured workers operating under hazardous conditions. Exports were directed primarily to Europe and North America to support agricultural intensification during industrialization. British firms controlled shipping, marketing, and chemical validation, while Peru retained ownership through a state monopoly operating via consignment contracts. This structure maximized short-term fiscal revenue but produced minimal domestic spillovers in technology, skills, or institutional learning.

From the 1870s onward, sodium nitrate extracted from the Atacama Desert replaced guano as the primary nitrogen input for fertilizers and explosives. The underlying production model remained unchanged: dependence on a single export commodity, reliance on natural resource rents, dominance of foreign capital, and weak economic diversification. The War of the Pacific (1879–1883) reallocated control of nitrate reserves, with Chile annexing Peru’s Tarapacá region and Bolivia’s coastal territory, including Antofagasta. Following annexation, nitrate exports expanded rapidly, reaching approximately 2–3 million metric tons per year by 1910 and generating up to 60% of Chilean central government revenue. Extraction imposed high environmental costs, including land degradation and water depletion. Labor demand drove large-scale migration from Peru and Bolivia, with total employment reaching roughly 70,000 workers by the 1910s. Public and private investment focused on ports (notably Iquique and Pisagua) and railways connecting extraction zones to export terminals.

As with Argentina during the same period, British capital dominated ownership, finance, and trade logistics in Chile’s nitrate sector. A substantial share of profits was repatriated rather than reinvested domestically. Chile supplied up to 80% of global nitrate demand for European and U.S. markets. State capacity improved selectively, particularly in customs administration, export taxation, and regulatory oversight of nitrate shipments. However, institutional development remained narrowly focused on extraction. Labor protections were weak, investment in industrial diversification was minimal, and public support for technical or scientific education was limited. Mining towns operated as closed systems under company control, including housing, retail supply, and wage payment through company stores. Employment levels, fiscal revenues, and urban growth were therefore tightly coupled to nitrate price cycles, leaving the economy exposed to external shocks, including the post–World War I collapse following the introduction of synthetic nitrates.

The Forces Behind Expansion and Collapse

Guano extraction exhibited limited technological variation due to its labor-intensive methods. In contrast, British-owned nitrate firms differed in size, processing approaches, logistics, and labor management. Firms adopted varying models for worker housing, compensation (cash wages versus company scrip), and transportation, particularly through railway integration. Most change occurred through expansion in the number of producing entities and consolidation rather than through innovation in extraction or processing technologies.

Global market selection mechanisms, institutional structures, and geopolitical pressures increased demand for nitrogen inputs as European agriculture and munitions production prioritized scale and cost efficiency. In the guano system, this favored low prices and high volumes. In Chile, export tax policy favored firms capable of sustaining high throughput. World War I temporarily increased demand for nitrates for munitions production. However, the commercialization of the Haber–Bosch process enabled synthetic nitrogen production at an industrial scale, rapidly eliminating the nitrate industry’s competitive advantage and market base.

Profitable nitrate practices became institutionalized, but spillovers into domestic manufacturing, chemistry, or engineering education remained limited. Investment patterns reinforced specialization in raw-material extraction rather than in capability development. As a result, Chile became locked into a single‑commodity trajectory, increasing systemic vulnerability to technological substitution and demand shocks.

Fiscal Capacity Without Transformation

The Peruvian state prioritized revenue generation over long-term development by maximizing guano rents without reinvesting in structural transformation. Revenues were centralized through a national monopoly and consignment system. Chile similarly relied on nitrate rents without articulating a diversification strategy or directing flows toward industrial upgrading. Neither state pursued value-added integration, such as linking nitrogen production to domestic agriculture, chemistry education, or human capital development. Fiscal capacity expanded, but political and social legitimacy eroded due to labor repression and visible inequality.

In Peru, state monopoly arrangements and exclusive contracts stabilized prices and volumes but constrained innovation. Public investment in railways and urban infrastructure supported extraction but not export diversification. Labor standards and resource stewardship received minimal attention. In Chile, export-oriented policy ensured stable property rights and predictable taxation for predominantly British capital. Significant public-private investment supported ports and railways servicing nitrate zones, but integration with the broader economy remained weak. Despite fiscal surpluses, funding for education, public health, and urban services remained limited.

The Peruvian state failed to account for depletion risk or the systemic vulnerability created by reliance on a single asset. Revenues were consumed or leveraged rather than saved or hedged. The resulting collapse triggered a fiscal crisis, sovereign default, and political instability, increasing Peru’s susceptibility to entering the War of the Pacific. Chile similarly underestimated fiscal dependence risks, consuming nitrate revenues without counter-cyclical planning. The collapse of the nitrate industry due to synthetic substitution led to mass unemployment, regional economic failure in Tarapacá and Antofagasta, and large-scale internal migration to Santiago and Valparaíso. The global economic collapse of 1929 amplified these effects. Unlike Peru, Chile used the crisis as a pivot toward state-led industrialization, expanded public ownership, and a strategic shift toward copper exports.

What Guano and Nitrates Still Teach Us

The history of guano in Peru and nitrates in Chile shows that development does not come automatically from abundance. Both countries built highly effective systems to extract, tax, and export natural resources. Roads, ports, railways, and state institutions expanded rapidly. Yet these systems were designed to export raw materials rather than to strengthen domestic capabilities. Education, industrial diversification, and technological learning were treated as secondary concerns—until it was too late.

When global conditions changed, the weaknesses became visible. Peru’s guano revenues collapsed with depletion, leaving the state financially fragile and politically unstable. Chile’s nitrate economy was destroyed not by exhaustion of the desert, but by a technological breakthrough abroad that made natural nitrates obsolete. Workers were displaced, entire regions declined, and public finances deteriorated. The difference between the two countries lies in their response: Chile eventually used the crisis as a turning point to pursue industrialization and new export sectors, while Peru lacked the institutional capacity to do so on the same scale.

For Latin America and the Caribbean today, the lesson is not to reject natural resources, but to treat them with caution and strategy. Extractive industries can generate revenue, but without deliberate investment in people, technology, and diversification, they also generate dependency and risk. The guano islands and nitrate deserts remind us that the real challenge is not how much wealth a country extracts, but whether it uses that wealth to prepare for a future in which the boom will inevitably end.