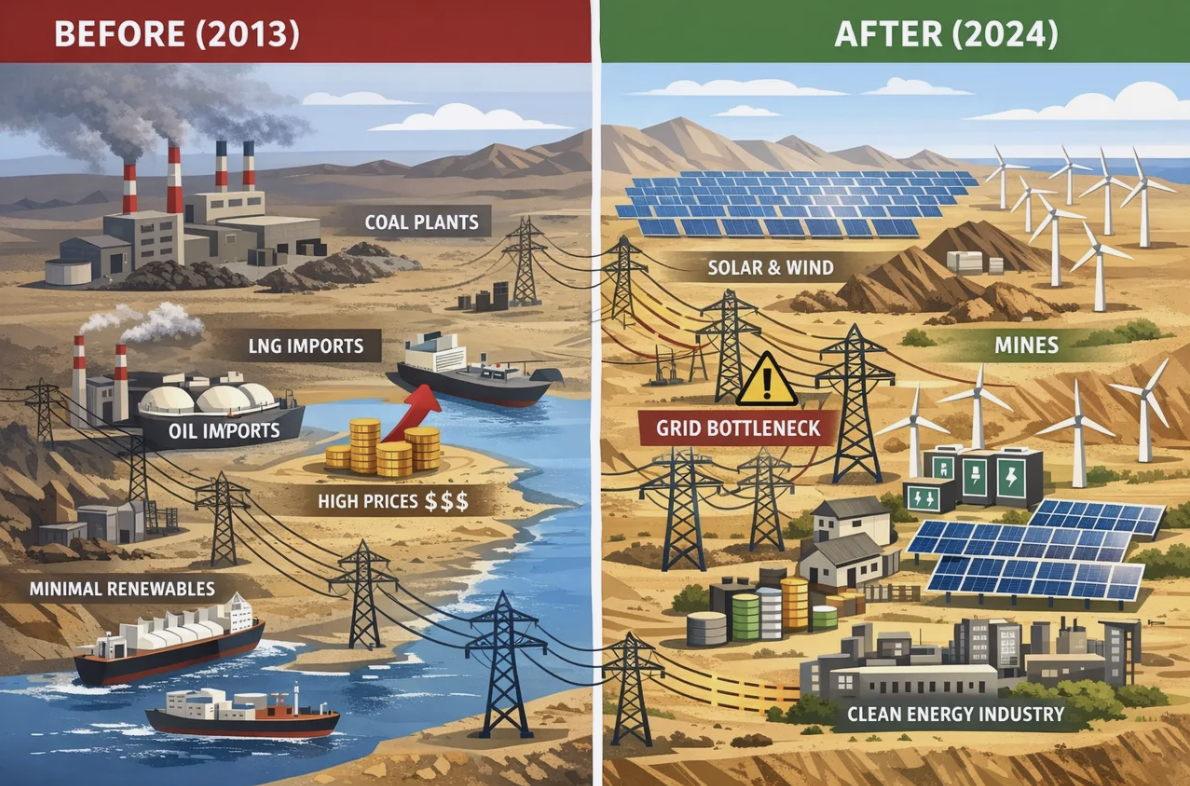

Chile shows that clean power can be a competitiveness strategy—not just an environmental commitment. In one decade, the country moved from about 63% fossil-fuel generation in 2013 to a system in which renewables provided about 70% of electricity in 2024, with solar and wind accounting for roughly one-third of national generation.

The hard part was not “getting renewables built.” The hard part was building systems that scale—grids, flexibility, permitting capacity, and social license—fast enough that cheap renewable power becomes usable power, not curtailed power. Chile’s experience makes this visible: solar and wind curtailment reached about 6 TWh in 2024, a warning sign that infrastructure and governance can lag private investment.

Chile’s transition was engineered through market design and state capability. Competitive auctions and long-term contracts drove prices down—bids reached US$13/MWh in the 2021 supply auction, with an average awarded price of US$24/MWh—and mining demand served as an anchor buyer through corporate power purchase agreements (PPAs). Transmission reform and institutional upgrades were aimed at keeping the system reliable as renewables grew.

For LAC countries, the prize is clear: lower power costs, stronger export competitiveness, and a credible path to transformation—without triggering backlash from communities or destabilizing the grid. This blog highlights what changed in Chile, why it changed, and why renewables won, and what the state did to turn private capital into scale, and where it still needs to catch up.

What changed: assets, money, power flows, and institutions

Natural capital – the Atacama Desert’s solar resources – was converted into installed solar photovoltaic (PV) capacity. Capacity grew from below 500 MW in 2014 to more than 13 GW in 2024. Wind capacity expanded from 1 GW to over 4 GW in the same period. Socio-economic capital deepened through investment and new industrial energy portfolios. By 2023, there was a pipeline of planned renewable investments that exceeded US$ 15B, mostly foreign direct investment in Atacama solar, transmission, and storage. Mining and energy firms built new, long-term portfolios of utility-scale PV, wind, and storage assets to address risks from imported fuel prices and stabilize energy supply. Chile shifted culturally and institutionally toward “green energy” and away from “energy scarcity.”

Energy flows were decarbonized—but also constrained by the grid. Chile reduced fossil-fuel import dependence. Fossil-fuel generation accounted for about 63% in 2013, and renewables reached about 70% by 2024. Yet the success of attracting finance for generation created congestion: renewable curtailment reached around 6 TWh in 2024, because low-cost supply outpaced transmission and grid flexibility. Finance shifted toward competitive pricing and new instruments. Chile attracted low-cost renewable energy finance and shifted from conventional project finance to green bonds and sustainability-linked lending. Auction design and long-term contracting led to dramatic price reductions—solar bids fell from more than US$100/MWh in 2013 to about US$13/MWh in 2021, reinforcing capital reallocation toward renewables. Knowledge flows accelerated through learning-by-doing and improvements in system operations—new capabilities formed in grid management, dispatch, and storage integration. By 2025, 1.7 GW of storage was operational or in testing, with more than 1 GW operational by mid-2025, deployed in part to mitigate curtailment challenges. Public-private partnerships (e.g., through Chile’s Economic Development Agency, CORFO) illustrate that Chile was not only importing technology but also adapting it to national and local operating conditions.

Market institutions were reorganized around auctions and corporate PPAs. Chile’s auction system and bilateral contracting (especially for large customers) became central in steering investment. Mining companies became major renewable buyers through corporate PPAs, turning industrial demand into an ‘anchor’ that reduced risk and accelerated scale. Technical institutions such as the Electricity Coordinator (CEN) and the National Energy Commission (CNE) strengthened planning and dispatch to modernize the energy system, but coordination gaps remained. The Energy Transition Law (2024) was intended to expedite the adoption of transmission and grid-forming technologies—an institutional response to system complexity. Social order shifted with new distributional tensions. While renewables improved air quality in coal-heavy regions and supported competitiveness through lower prices, the changes led to conflicts over land use, transmission corridors, consultation, and water governance—especially in the Atacama Desert.

Why things changed: experimentation → market selection → rapid scaling

Chile’s transition began with competing pathways to energy self-sufficiency: coal expansion, liquefied natural gas imports, and renewables. Over the decade, the system tested utility-scale PV, onshore wind, and concentrated solar power with storage, such as Cerro Dominador, as well as small-scale distributed generation projects (500 kW–9 MW) under stabilized pricing regimes. Hybrid projects pairing renewables with 4-hour battery energy storage systems also emerged to address intermittency. Policy innovation produced ‘institutional variation.’ A key reform was the auction redesign (2014 onward), which allowed renewable providers to bid into specific time blocks, enabling solar to compete with 24/7 thermal generation on a more comparable product basis. Spatial variation mattered: Atacama’s resource strength attracted mass deployment but also highlighted the importance of siting, grid access, and social license, leading to uneven project outcomes across different regions.

Cost-based selection strongly favored solar and wind. Competitive auctions and corporate procurement revealed solar as the cheapest scalable option; coal and other thermal assets lost viability when solar prices dropped to around US$13/MWh in 2021. Environmental and political selection accelerated coal decline, including through coal phase-out agreements accompanied by just transition strategies for communities. By 2024, 11 plants, or about 1.2 GW of coal capacity, had been retired or converted, reflecting both the direction of climate policy and shifting economics. Industrial selection, especially from mining, is reinforcing the case for renewables. Large mining firms (e.g., Codelco and BHP) selected renewables to lower costs and meet emerging ‘green copper’ demand, making export competitiveness a direct selection pressure.

Technology diffusion was rapid: solar and wind spread from Atacama/northern corridors toward central Chile as capabilities and financing templates matured. Storage diffusion followed the pressures that arose from curtailment. Institutional diffusion also occurred: the ‘Chilean model’ of auctions has been studied and adapted by other LAC countries (e.g., Colombia) to de-risk renewable energy pipelines. Diffusion depended on enabling infrastructure. Major transmission projects, e.g., the 1,500 km Kimal–Lo Aguirre line, were considered public goods and designed to connect Atacama solar to central demand. Diffusion thus required both market signals and grid build-out.

What the state did: markets, grids, risk, and legitimacy

Chile used long-horizon planning and policy to provide a ‘North Star’ for investors and agencies. Energy 2050 is a state policy designed to outlast political cycles, in line with the direction set by the Framework Law on Climate Change. The state’s coordination role was essential because the climate transition is cross-sectoral. Energy policy interacted with mining competitiveness, environmental justice, and territorial governance; government convening and planning capacity shaped the pace and credibility of the transition. Where coordination lagged—especially between generation growth and grid expansion—system costs rose through congestion and curtailment, underscoring the state’s responsibility for sequencing reforms and infrastructure.

Technology-neutral auctions rewarded the lowest cost and created transparent price signals. Auction reforms and time-block design enabled renewables to compete credibly and delivered price discovery that reoriented investment away from fossil options. Grid access and system rules evolved to support higher variable renewable penetration. Changes included stronger technical agencies (CEN and CNE), modernization of the national energy system, and reforms to allow non-discriminatory grid access and stabilized pricing for smaller developers. Environmental and social standards were both enabling and constraining. Chile worked to streamline permitting and develop standards (e.g., green hydrogen certification and environmental impact assessments). But uneven local impacts—water use, land conflict, and Indigenous consultation—show that standards and enforcement capacity must scale with deployment.

Transmission reform was a decisive state intervention. The 2016 transmission law enabled long-distance solar integration, and the state treated major projects (e.g., the US$2B Kimal–Lo Aguirre high-voltage direct current line) as public goods essential for the transition. Public risk absorption catalyzed early investments and first-of-a-kind projects. Blended finance and early risk-sharing, including through state instruments and development finance, e.g., the Cerro Pabellón geothermal project, reduced barriers until private finance scaled. Innovation ecosystems were actively fostered. CORFO supported research and development and concessional finance for first-of-a-kind green hydrogen facilities and public-private initiatives, building Chile’s capacity to deploy and partially adapt technologies rather than only import them.

The LAC takeaway: build systems that scale

Three headlines from Chile’s decade:

· Market design can unlock scale. Technology-neutral auctions and bankable long-term contracts made renewables investable and drove dramatic price discovery.

· Competitiveness anchors transitions. Mining demand and corporate PPAs helped convert renewable potential into real investment and industrial advantage.

· Success creates new challenges. When grid expansion and flexibility lag, abundance becomes waste: solar and wind curtailment in 2024, demonstrating that the transition’s bottleneck shifts from “building MW” to “integrating MW.”

For LAC policymakers, some key lessons include that well-designed auctions and contracts can reward low-cost generation and deliverability; investing early in transmission and grid system flexibility as public goods prevents the grid from becoming a constraint; and building permitting and consultation capacity so projects have social license at the pace needed for deployment – legitimacy is as critical as finance.

It is not just about building more renewables – but about building systems that value reliable renewables and make them politically durable.