Many industrial policies share a common flaw: they are designed for success and unprepared for failure. Subsidies get extended, protection becomes permanent, and development banks accumulate risk without a clear plan to exit. Taiwan and South Korea’s experience between roughly 1955 and 1990 offers a structurally different model. In one generation, both converted agrarian economies into world-class exporters—showing that late-industrializing states can scale manufacturing capabilities rapidly when policy ambition is matched by institutional discipline.

The core mechanism was not simply “more state,” but concentrated state authority over credit and trade, paired with hard performance tests. Governments steered finance, foreign exchange, and incentives toward priority sectors—and then used export results, investment targets, and periodic restructuring to cut losses and redirect capital when bets failed. Its relevance today lies in what both states got wrong as much as what they got right: rapid gains that concentrated risk, requiring painful restructuring later. Korea’s heavy and chemical industries’ rapid expansion in the 1970s produced overcapacity and non-performing loans that contributed to the 1979–80 crisis, followed by restructuring. Taiwan faced mounting pressure in the 1980s as labor-intensive exports lost competitiveness, forcing upgrading.

The lesson for LAC is therefore less about replicating Korea’s conglomerates or Taiwan’s SME networks than about building the public-finance and planning routines that make industrial policy reversible: clear objectives, measurable milestones, and credible exit and restructuring rules. In both economies, instruments evolved over time—shifting from tighter vertical targeting toward more horizontal, capability-building policies in the 1980s—without abandoning outward orientation. Korea eased its most directive tools and restructured chaebol after 1979–80; Taiwan adopted a 10‑year economic plan in 1980 to steer upgrading toward technology‑intensive sectors. The sections that follow document what changed, what drove it, and how the state governed the process.

What changed (1955–1990): the shape of structural transformation

Industrialization shifted capital stocks from agriculture toward manufacturing and tradable industry. This reallocation was reinforced by outward‑oriented flows of goods, finance, and knowledge. Export earnings financed the import of machinery, thereby raising productivity and enabling further investment. Rising domestic savings deepened this accumulation loop. In Korea, commodity trade expanded from roughly US$480 million in 1962 to nearly US$128 billion by 1990, while domestic savings rose from about 3 percent of GNP in 1962 to over 35 percent by 1989. In Taiwan, exports accounted for a large share of non‑food manufacturing growth in the 1960s, and total trade increased nearly tenfold in the 1970s.

Both states rebuilt social institutions to support export‑oriented industrialization. Planning agencies, trade regimes, and financial systems were redesigned to privilege industrial upgrading. Control over banking and foreign exchange allowed governments to steer investment toward priority sectors. Institutional designs diverged in form but not in intent. In Korea, five‑year plans, the National Investment Fund, and the Korea Development Bank channelled credit to steel, shipbuilding, machinery, petrochemicals, and electronics after 1973. In Taiwan, exchange rate reform in 1958–1960, export processing zones in the 1960s, and a 10-year economic plan adopted in 1980 structured export promotion and technology upgrading.

Structural change reshaped social coalitions and distributional outcomes. Export‑oriented growth expanded urban employment and new middle classes while reducing agriculture’s economic role. At the same time, sectoral and regional disparities intensified. Periodic crises forced the renegotiation of coalitions. In Korea, factories in Seoul and surrounding regions accounted for nearly half of manufacturing value added and employed almost half of factory workers by the late 1970s. In Taiwan, sugar and rice declined to about 3 percent of exports by 1970, shifting rents and political influence toward industrial and small to medium-sized enterprise interests. For LAC, this political-economy channel is not incidental: reform efforts—from phasing out agro-industrial protection to restructuring energy subsidies—often fail or stall when governments underestimate how quickly rents and regional power bases shift during structural transformation.

What drove the changes: experimentation, selection, and upgrading

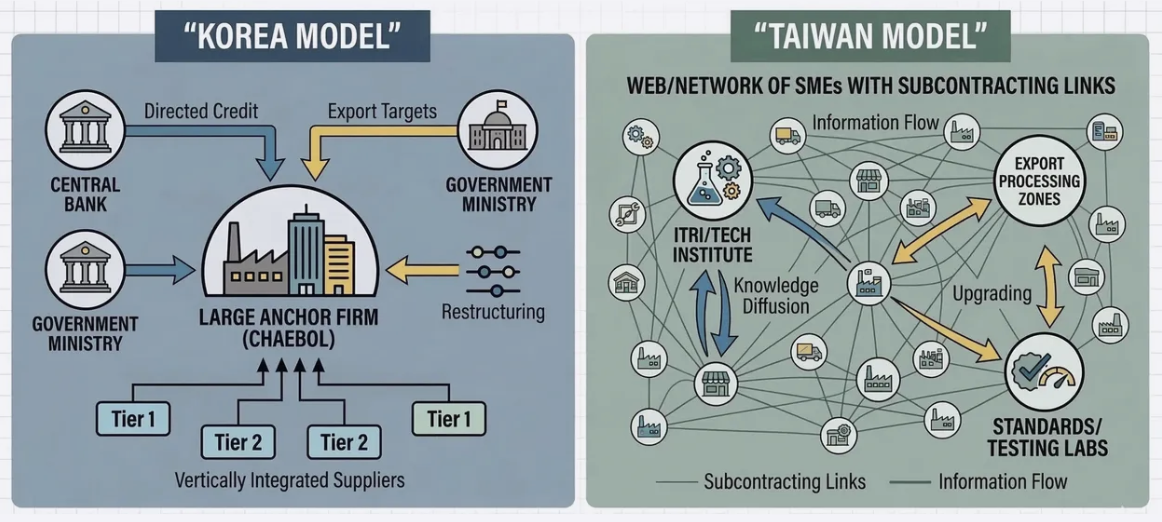

Both economies generated variation through policy and organizational experimentation. Early import‑substitution strategies were tested and then abandoned as constraints emerged. Export promotion created new competitive environments that encouraged further experimentation. The analytically powerful contrast is that Korea and Taiwan converged on the same goal—solving the coordination problems of scale, finance, and capability upgrading—through two divergent firm structures. Taiwan’s export boom was coordinated through dense networks of small and medium-sized firms (SMEs) and flexible subcontracting. At the same time, South Korea solved the same scale‑and‑coordination problem through large, vertically integrated chaebol (large, family-controlled conglomerates organized as diversified groups of affiliated firms, historically supported by close ties to state-directed finance) backed by state‑directed credit. This is not a historical curiosity; it maps directly onto a live LAC design tension: whether states should back national champions (e.g., Brazil’s BNDES-style approach; Chile’s large copper firms) or build ecosystems that help many smaller firms scale (e.g., the Dominican Republic’s export processing zones; Costa Rica’s tech‑linked upgrading). The lesson is not that one structure is universally superior, but that each requires different instruments to coordinate investment—and different forms of discipline to prevent support from becoming permanent.

Selection operated through state‑mediated credit allocation and international markets. Access to subsidized finance depended on meeting export and investment targets. World‑market competition filtered out firms and sectors unable to meet price and quality standards. Political reassessment followed failure. In Korea, subsidized credit was rationed through state‑controlled banks and withdrawn from underperforming firms during the 1980s restructuring. In Taiwan, preferential credit, tax incentives, and access to export processing zones rewarded firms that succeeded in export markets. Once successful, export‑oriented industrialization diffused and became entrenched. Institutional routines reduced the cost of repeating outward‑oriented strategies. Learning by doing and sunk investments created path dependence. Core features were adjusted but not abandoned. Taiwan’s growth acceleration began around 1962 and lasted for more than three decades, with real GDP growth averaging roughly 8–9 percent per year through the early 1980s. Korea maintained an export-oriented approach from the early 1960s through the 1980s, despite scaling back vertical industrial policies after the 1979–80 crisis.

How the state guided change: credit, trade, and discipline

The state provided clear direction and engineered market rules to align private incentives with national goals. Strategic coordination was exercised through multi‑year plans and central agencies. Trade and exchange‑rate regimes were redesigned to favor exports. Regulatory architectures shaped firm behavior. Korea’s Economic Planning Board, created in 1961, coordinated five‑year plans and export targets across ministries and banks. Taiwan’s exchange rate reform in 1958–1960 and the export promotion statutes of the 1960s restructured market incentives toward outward orientation.

Public investment provided the infrastructure and human capital needed for industrial-scale production. Both Taiwan and Korea expanded technical and vocational training—and strengthened engineering education—to match the skill needs of export manufacturing and technology upgrading. State‑controlled finance mobilized savings and absorbed risk in priority sectors. These interventions enabled large, long‑gestation projects. They also concentrated fiscal and financial exposure. In Korea, public and public‑enterprise investment accounted for roughly 40 percent of total domestic investment between 1963 and 1979, with major spending on power, ports, and transport. Korea’s domestic savings rate rose from 3.3 percent of GNP in 1962 to 35.8 percent by 1989, channelled through controlled banking systems into industry.

Innovation systems emerged through learning‑by‑doing within export‑oriented ecosystems. Acquisition and adaptation of technology were prioritized over frontier invention. Organizational forms shaped how learning diffused. Policy feedback adjusted support mechanisms over time. In Korea, targeted support for steel, shipbuilding, and electronics enabled chaebol to become global players by the mid‑1990s. In Taiwan, public technology institutions—most notably the Industrial Technology Research Institute (ITRI)—helped absorb foreign know‑how, incubate new capabilities (especially in electronics), and diffuse process and design improvements across networks of SMEs.

The practical implication for LAC is not a single template but a shared design principle: the organizational form matters less than the discipline built around it. Korea’s chaebol and Taiwan’s SME networks succeeded not because one structure is superior, but because each was embedded in credible performance tests—and governments were willing to act when those tests were failed.

Implications for LAC

For finance and planning ministries, the Taiwan–Korea comparison is most relevant as a lesson in state capacity to coordinate investment under hard budget constraints. Both countries solved early coordination failures by steering credit, trade incentives, and planning priorities—but they did so with clear performance tests and a willingness to restructure when bets went wrong. The LAC takeaway is that any modern industrial or productive‑development push (nearshoring, energy transition, strategic minerals, advanced services) must be designed as a fiscally legible program: explicit objectives, quantified milestones, transparent costs (including tax expenditures), and a credible plan to manage fiscal risks arising from public banks, guarantees, state-owned enterprises, and public-private partnerships.

A second implication is to recreate “export discipline” using instruments that sit squarely within finance and planning systems. Rather than open-ended protection, support should be conditional and time-bound—linked to verifiable indicators such as export survival, productivity, formal job creation, certification/quality adoption, and integration into higher-value-added segments of value chains. Ministries of Finance can operationalize this through results-based transfers and credit lines, rules for tax incentives (ex-ante costings, publication, and periodic review), and procurement that rewards performance and innovation while preserving competition. Planning ministries can align these tools with a national investment pipeline and a small set of priority missions that are revised as capabilities change.

Finally, the institutional lesson is to treat structural transformation as a governed portfolio of experiments. For finance and planning authorities, the priority is not picking winners once but building routines to allocate, monitor, and exit public support in a way that protects the sovereign balance sheet. That, in turn, means agreeing on a single results framework with a short list of metrics; funding independent evaluation and public reporting; writing sunset clauses and restructuring triggers into programs from the outset; and maintaining fiscal-risk oversight of development banks, SOEs, and PPPs—including stress tests and caps on guarantees. Done well, this shifts LAC policy from ad hoc deals toward credible commitment: investors get stability and coordination, while governments retain the ability to correct course when external conditions tighten.

Taiwan and Korea show that state-led transformation is possible—but not as a permanent arrangement. Both states eventually had to let go of favored sectors, protected firms, and comfortable credit concentrations. The question for LAC is not whether governments can pick priorities, but whether they can build the institutional reflexes to revise them. That capacity doesn’t emerge from good intentions. It must be designed from the start.