In August 1972, oil began flowing through a newly completed pipeline across the Andes, and Ecuador’s economy changed almost overnight. Between 1972 and 1981, the country experienced one of the fastest growth episodes in its modern history, driven by the sudden start of large-scale oil exports. Real GDP grew at close to 9 percent per year, while exports and government revenues expanded sharply within a few years. The same period also locked in a larger state, higher public spending, and rising external debt that proved difficult to reverse.

The transformation began in August 1972 with the completion of the Trans‑Andean oil pipeline linking Amazon oil fields to the Pacific coast. Oil rapidly accounted for more than half of total exports, bringing total exports to roughly a quarter of GDP. Central government expenditure doubled as a share of GDP, while public foreign debt increased almost eighteenfold by 1981. Manufacturing output also grew rapidly in the mid-1970s, as oil revenues allowed the state to scale up import-substitution policies already in place.

The central policy implication is that Ecuador’s oil boom reshaped the entire economic and institutional ecosystem, not just the export sector. The sections that follow examine how capital stocks, institutions, and social structures changed during the period. They then explain how these changes unfolded through variation, selection, and diffusion. Finally, they assess how state action directed, financed, and adapted to the transformation.

Oil Rents: Capital, Institutions, Society

The oil boom fundamentally altered Ecuador’s capital stocks by rapidly expanding physical and financial assets tied to extraction and public investment. The 503‑kilometer Trans‑Andean pipeline, completed in 1972, enabled commercial oil production at scale for the first time. Oil revenues financed large public investments, with capital expenditure averaging about 17 percent of government spending and directed mainly to highways, hydroelectric plants, and state enterprises. Financial capital also surged as oil accounted for roughly one‑third of central government revenues and generated large foreign‑exchange inflows in the early years. At the same time, external sovereign borrowing replaced foreign direct investment as the main external capital flow, pushing public foreign debt from US$248 million in 1971 to more than US$4 billion by 1981. Natural capital was drawn down rapidly through oil extraction in the Amazon, while environmental costs were not reflected in fiscal or investment decisions during the period.

Institutional change accompanied the rapid accumulation of oil‑based capital. The 1971 Hydrocarbons Law declared hydrocarbons to be inalienable property of the state and laid the legal foundation for state control of the sector. In 1972, the government established the state oil company, CEPE. It progressively increased its ownership stake in the main oil consortium, reaching 62.5 percent by 1977 after buying out Gulf Oil. Planning and coordination functions were strengthened through JUNAPLA, Ecuador’s national planning body, which allocated oil revenues to infrastructure and industrial projects. The Industrial Promotion Law structured import‑substitution incentives, offering duty exemptions on capital goods and protection from imports for favored industries. These institutions expanded the state’s role in directing investment decisions across the economy.

The oil‑driven expansion reshaped Ecuador’s social and economic structure. Urbanization accelerated as public investment in roads, electricity, and water created construction and service jobs, drawing labor from rural areas. Agriculture’s share of GDP and employment declined, while construction, services, and manufacturing expanded. Public sector employment grew rapidly as ministries and state enterprises expanded payrolls, broadening urban wage employment. Distributional effects were uneven: urban wage earners benefited from rising public and industrial employment, while rural incomes lagged, and agrarian reform redistributed only a small share of cultivable land. Inflation averaged around 13 percent per year, eroding fixed incomes and placing greater pressure on poorer households.

New Activities, Policy Selection, Lasting Effects

The period introduced economic activities and organizational forms that had little precedent in Ecuador. Large‑scale oil extraction in the Amazon and pipeline transport across the Andes represented an entirely new production system. The creation of CEPE marked a shift from concession‑based oil development to a state‑led, joint-operations model. Import-substitution manufacturing expanded under tariff protection and capital goods subsidies, encouraging the establishment of new factories producing consumer goods and intermediate inputs. Ecuador’s accession to OPEC in 1973 integrated the country into a global oil governance regime that influenced pricing and production norms. Together, these changes increased the diversity of economic activities, though many relied heavily on state support.

Selection mechanisms during the boom were driven primarily by policy and external shocks rather than market competition. The Hydrocarbons Law and subsequent decrees forced most foreign oil companies to relinquish concessions, leaving CEPE and its remaining partner as the dominant producers. The 1973 global oil price shock sharply increased oil export rents, reinforcing state control and dependence on petroleum revenues. Industrial policy sheltered manufacturing firms from competition, selecting activities based on access to incentives rather than efficiency or employment generation. Political events also mattered: disagreements within the military government over the pace of nationalization and fiscal expansion contributed to the 1976 leadership change, after which the expansionary model continued but with some moderation. These filters favored capital‑intensive, protected sectors while weakening traditional agriculture.

Many features of the oil‑era transformation persisted beyond the boom years. Central government expenditure remained at roughly double its pre-1972 share of GDP even after oil prices fell, indicating strong downward rigidity. CEPE’s dominant role in oil production was consolidated through successive equity acquisitions, institutionalizing state control of the sector. Import‑substitution policies and planning institutions remained in place through the late 1970s, even as fiscal pressures mounted. By contrast, there is little evidence that systematic learning led to major course corrections during the boom, such as saving oil revenues or restructuring incentives. The diffusion of oil‑financed infrastructure and public employment created lasting expectations about the state’s role in development.

State Policy: Investment, Regulation, Debt

The state played a decisive role in directing the transformation through laws, regulations, and strategic choices. The Hydrocarbons Law of 1971 redefined ownership rights and enabled the state to retroactively restructure contracts. Subsequent decrees enforced territorial relinquishment by foreign companies and empowered CEPE to operate across the oil value chain. Trade, investment, and labor regulations were used to support import substitution, limit foreign ownership in selected sectors, and manage wages and working conditions. Ecuador’s participation in OPEC further embedded state involvement in determining export conditions. These measures provided a clear signal that oil rents would be centrally managed and deployed to support development objectives.

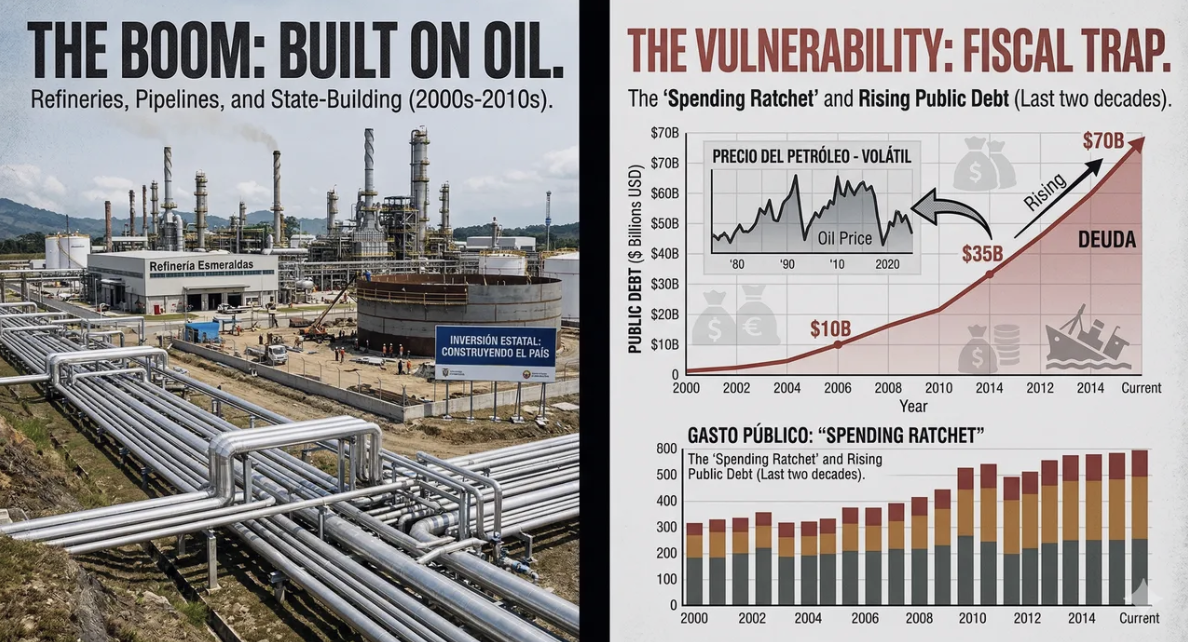

Oil revenues allowed the state to become the economy’s principal investor and coordinator. Public capital spending expanded rapidly, financing highways, hydroelectric plants, refineries, and urban infrastructure that reshaped production and settlement patterns. The Esmeraldas refinery, which began operations in 1978, exemplified state‑directed industrial investment linked to oil extraction. Credit allocation through public banks and development funds supported favored sectors, while fuel subsidies and public employment sustained urban consumption. When revenues proved insufficient to match spending ambitions, the government relied on abundant international liquidity to borrow externally at low interest rates. This strategy mobilized resources quickly but increased vulnerability to future shocks.

Evidence of adaptive policy management during the boom is limited. Despite rising inflation, growing imports, and mounting debt in the late 1970s, fiscal expansion largely continued. Some adjustments occurred, including currency devaluations and price increases toward the end of the decade, but these did not reverse the underlying spending trajectory. The absence of a stabilization or savings mechanism meant that oil windfalls were fully spent rather than smoothed over time. Institutional learning within CEPE and the industrial promotion system appears to have been slow, with operational inexperience and incentive misalignment persisting. As a result, the state entered the early 1980s with a larger public sector, heavy debt burdens, and limited buffers.

Lessons for LAC Policymakers

Ecuador’s 1972–1981 oil boom delivered rapid growth while transforming institutions and social structures. Oil exports and prices generated unprecedented revenues that financed infrastructure, industrial expansion, and a larger state. These gains were accompanied by rising debt, inflation, and uneven distributional outcomes. Many institutional changes proved durable even after the boom ended.

The experience illustrates a development path in which resource rents accelerate accumulation but also entrench rigidities. A larger public sector, centralized control over strategic resources, and protected industries became defining features of the economy. Infrastructure and urbanization gains endured, while diversification and human capital development lagged. The legacy was an economy more complex than before 1972, but also more exposed to fiscal and external shocks.

Over the longer run, the boom left Ecuador with a state-growth model structurally tied to oil rents. The infrastructure and expanded public administration created real capacity, but they also raised the economy’s break-even fiscal needs and hardened expectations around subsidies and public employment. When oil prices fell or external financing tightened, adjustment pressures surfaced through debt stress, stop‑go public investment, and renewed conflict over how to distribute and govern the rent. In this sense, the boom’s central legacy was not only faster growth in the 1970s, but a durable pattern of procyclical policy and volatility anchored in petroleum wealth, reinforced by oil-rent institutions built under military rule in the 1970s.

For LAC governments managing resource windfalls today—whether from oil, gas, copper, or lithium—Ecuador’s record offers three specific warnings grounded in the evidence. First, the design of industrial incentives matters more than their scale: Ecuador’s Industrial Promotion Law channelled capital into protected factories that generated few jobs and depended permanently on state support, because the law rewarded capital intensity rather than employment or productivity. Getting incentive design right at the outset is far harder to fix once firms and lobbies have organised around the existing structure. Second, fiscal expansion during a boom is a one-way ratchet: central government spending doubled as a share of GDP. It never reversed, because the political cost of cutting it proved insurmountable once expectations were set. Stabilization funds must be established at the start of the windfall, not its end. Third, ownership transfer must be sequenced with capacity building: CEPE was handed majority control of Ecuador’s oil sector before it had the technical experience to run it, slowing exploration and operational efficiency for years. Venezuela faced the same challenge in the same decade with PDVSA. The lesson is not to avoid state ownership but to invest in institutional competence before, not after, transferring control.